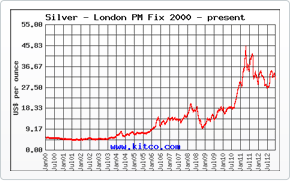

Gold and silver will finish the week posting losses, but things are much better than what they could have been and what they were a week ago. All in all, this week saw the focus of the market placed entirely on US economic data, but there were a few rumblings in Asia that the investing world felt it necessary to pay attention to. Despite such a large slate of US economic data, it was only a report or two that really caught the eyes and ears of investors.

Across the globe, things have quieted down considerably now that we no longer have the Greek debt debacle or Iranian Nuclear Deal to worry about. The USD and euro have become sparring partners once more, but as has been the case for the past few months the greenback is the better of the two as far as performance and future outlook is concerned.

Chinese Equities Hurt US Equities

A theme that has been found over the past few trading weeks is one that shows an extremely unstable Chinese equity market. Stocks in China have been up and down for the past month or so, and the general downward movement of the Chinese stock market has been dragging down other global equity markets as well.

Though US stocks are performing well at present, they too are feeling the stress of China’s instability. This is why we have seen US stocks fluctuate at times over the past few weeks. All in all, however, the US economic picture is a bright one and is only continuing to improve with each passing week.

Heavy Slate of US Economic Data

The biggest piece of economic data made public this week came on Thursday in the form of the GDP report from the US’ second quarter. Officially, the GDP data came back about in line with expectations and was generally upbeat. With most people overlooking the data from this year’s second quarter, it gave them time to focus on a revision made to first quarter GDP data.

According to the revision, US first quarter GDP ticked upward by nearly 3%, despite previous predictions holding that the US economy grew by less than on half of one percent. This data was heralded as a big success considering most looked back at this year’s first quarter in disappointment.

The news was not all good from the US as investors saw pending home sales and consumer confidence dip noticeably in June. These two pieces of data were considered by the investing world, but were generally overlooked as the GDP data is much more heavily weighted in the eyes of investors.

This week also played host to July’s FOMC meeting, which wrapped up Wednesday afternoon. Wanting to hear more with regard to pending interest rate hikes, the market paid close attention to anything and everything Janet Yellen had to say in her post-meeting statement. Unfortunately, in typical Fed fashion, Ms. Yellen did not offer much in the way of actual insight with regard to interest rate hikes. Instead, she and her colleagues maintained that the US economy is continuing to improve and will be ready for interest rate hikes when the time comes.

Looking ahead to next week, I imagine that we will see the market focus on US equities, the USD, and just about anything else pertaining to the US economy. There are many factors that may affect the raising of interest rates, but at this point hikes are more or less expected to happen come September or October.