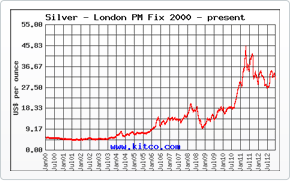

Precious metals began the week posting some decent gains, but by Wednesday that had all changed as losses began to mount thanks to stronger stocks and a stronger Dollar. Though Friday will see both gold and silver finish the week on a positive note, there is not much in the way of gains that can be taken away from this past 5-day trading session.

There were some comments from members of the Federal Reserve with regard to what they think should be done to interest rates, and to the surprise of many, many of them were in favor of raising rates sooner rather than later. The one thing that all of these Federal Reserve presidents had in common, however, was the fact that they have no voting rights on the FOMC—meaning they have no influence as to when rates will be raised nor how drastically they will be raised by. So while it is nice to hear members of the Fed confident that the US economy is in such a position that rates can be raised, it must be kept in mind that the opinions offered from these Fed members are nothing more than their own thoughts and beliefs and don’t necessarily reflect what the future holds for interest rates.

Slate of US Economic Data Dealt This Week

The US economy was dealt a mixed bag of economic news this week as it was reported that consumer prices during the month of March rose just barely, and by margins that were smaller than expected. As far as inflation reaching the 2% goal set forth by the Fed, figures such as March’s consumer prices do not exactly lead one to believe that the 2% goal is a realistic one. With that being said, it is important to remember that we are still only ¼ of the way through the year.

On the other side of the coin was the weekly jobless claims report, which indicated that 13,000 fewer first-time unemployment claims were filed last week than the week preceding it. This means that the seasonally adjusted average number of jobless claims has moved down to a reading of 253,000, despite expectations that we would once again meet or eclipse the 270,000 mark this week.

All in all, the US employment sector is performing well and has been for some time. Now, we are inching in on 60 consecutive weeks where jobless claims, on a seasonally-adjusted basis, have remained below the 300,000 mark.

IMF Downgrades Global Growth Forecast

In a statement made earlier in the week, the International Monetary Fund downgraded their projections for annual global growth. Despite December projections of annual growth just barely short of 3.5%, we are now looking at projections that show the global economy growing just barely more than 3%. This statements comes in the wake of first-quarter economic data that largely missed the mark and showed that most parts of the world had a rough first three months of the year.

Contributing factors to the IMF’s expectations that conditions will not improve at a fast rate are an energy sector that has been beaten to pulp in recent months. Not only has crude oil experience free-fall after free-fall, we just heard this week that one of the United States’ biggest suppliers of coal energy has declared bankruptcy and is doing away with thousands of jobs. As the world attempts to make the transition from fossil fuels to more sustainable sources of energy, the energy sector will continue to take a beating.

It will be interesting to see, over the coming weeks, just how the marketplace responds to monthly meetings held by the FOMC and the ECB. Though most have already discounted the possibility of a rate hike in April, there is still a strong contingent that believes at least one rate hike will happen by or before June. Some of this school of thought’s biggest believers are presidents of US Federal Reserve banks.